India's FinTech scene: UPI

India's FinTech scene: UPI

View from the trenches of Unified Payment Interface

At the top of 2024, I was in Asia visiting India and Sri Lanka. During my visit to India, I had no different observations from what several others have already had. Some of the major noticeable ones being: heavy mobile penetration, access to high-speed internet, digitization (cashless society) besides other things (like accelerated urbanization, energized youth, growing entrepreneurship, investment in infrastructure etc.). But for the purposes of this article let’s focus on mobile, digitization, high-speed internet in a cashless society.

What does high mobile penetration, digitization, high-speed internet in a cashless society in a the fastest growing GDP country lead to → increase in commerce which drives innovation in payment infrastructure. Enter UPI.

What is UPI?

A Unified Payments Interface (UPI) is a payments protocol built on top of a bank to bank retail payment system, Immediate Payment Service (IMPS) that allows users to transfer money between bank accounts. It is developed by the National Payments Corporation of India (NPCI), and it eliminates the need to enter bank details or other sensitive information each time a customer initiates a transaction.

If you have never heard of UPI here are some great starter articles on UPI:

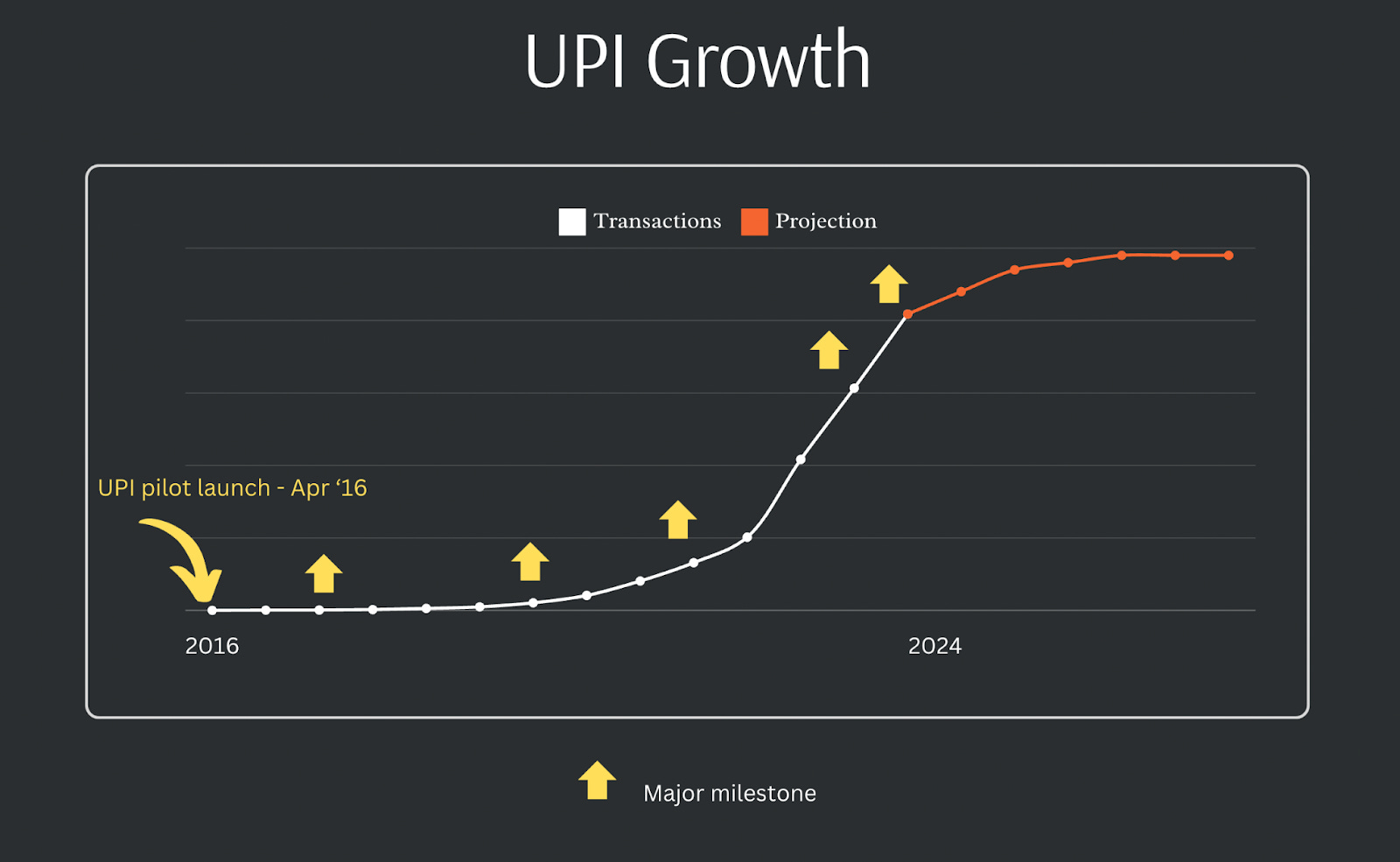

Suraj posted this thread on Twitter (X) in 2022 when UPI hit a huge milestone $1T

Here are official App Stats from NCPI

Media articles

Ranging from a 1B+ daily transactions to countless more, one can find several articles on the achievements of UPI; It really is a marvel. However, we are taking a look at what investments when done right can take this S curve of growth back to’ up and to the right’. For this, I have partnered with my co-author Mandar Kagade, founder - Principal at Black Dot Public Policy Advisors, an Indian ‘K Street’ firm focussed on financial services.

Background on UPI: UPI was inaugurated in 2016. Demonetization was framed as an anti-corruption measure to end black money in politics, bureaucracy etc. However, that did not work, so the proponents pivoted to the narrative that demonetization was also motivated by digitizing payments. UPI fitted the narrative squarely. UPI adoption (in the critical 0 to 1 stage)1 benefited from this tailwind. However, growth has plateaued out at 300 million active UPI users2 in a population of 1B in india. There are several factors driving this slowdown including infrastructural. We could tabulate them as follows without being exhaustive:

UPI landscape, usage trends & infrastructure

Macro infrastructure3

Internet penetration growth: 8 %

Overall smartphone market growth: 7-8 %

4G feature phone growth: > 10 % in 2024

5G Smartphone growth: > 40 % in 2024

VFM4 Smartphone growth: > 300 % YoY

The Union (federal) Government prohibited levy of any charges in the nature of interchange on UPI circa 2021, to both shield micro and small businesses from incurring transaction charges and bringing India’s large informal economy into the formal fold. This statutory prohibition on interchange on UPI means payment system participants do not have enough revenues they can plough back into acquiring more merchants and bringing in more users into the UPI fold.

The appetite for spending to acquire and retain consumers for repeat business is lower presently relative to in the first 3 years.

Tier 2, 3, 4 etc towns/villages have lower trust due to illiteracy & lack of financial knowledge.

Solutions for the Next 300M users

UPI lite

Relax MDR restrictions

Credit as a hook

UPI lite: UPI lite is a feature within the UPI to process small payments offline and non-real time to reduce the overload (given high volumes) on banks’ core banking system. UPI lite in effect is an on-device wallet that mimics a cash transaction at the point of sale.

As the mobile infrastructure data5 reproduced above suggests, internet penetration growth is a mere 8 %. Since the conventional UPI product is a RTP, it requires the internet to sustain its incremental user growth.

UPI lite could be one potential option to solve for this tension. Besides mitigating the ‘technical declines risk’ by enhancing redundancy within the UPI ecosystem, its offline functionality can be a lever to end-run the slowing growth of internet penetration (and relatedly, the choppiness of it as well).

However, UPI lite transaction cap is INR 500/- relative to the average ticket size on UPI (INR 1500/-), ticket size cap on UPI lite needs to be meaningfully high to allow for at least one grocery run for it to proliferate. At present, being 3x lower than the median ticket, it cannot support staples use-cases (like groceries). NPCI and RBI might want to consider UPI lite as a solution for the slow growth of telecom infrastructure conundrum6.

Relax MDR restrictions: This one is plain. The revenue can be plowed back to acquiring more merchants, more consumers and generally, financial trust and education initiatives by the PSPs.

Credit as a Hook: The RBI has since 2021 pivoted to leveraging UPI as a highway for delivering low ticket credit to consumers and thereby enhancing adhesion between merchants and UPI (through higher AoVs). Both Rupay credit card and a credit line product that banks can offer are the available vectors.

If the PSPs (banks in this context) have the right incentives, credit can be a hook for greater stickiness on both sides of the UPI loop and bring in the incremental (next) 300 million user base to UPI. Early days but data suggests the Rupay credit card has a lot greater traction than does the credit line offering. The ‘fix’ could lie in allowing non-bank financial companies7 to issue credit lines on UPI. But that is a heavy cultural lift for the RBI given it is a conservative Institution and legally, NBFCs are not PSPs (simply put, NBFCs cannot be members of a payment system without regulatory reforms).

Dominance of a Minority of Third Party Payment Applications

Another issue that policymakers have been grappling with in connection with UPI is the concentration of volumes in the top 2 or 3 TPAP8s. In response, the NPCI proposed a ‘market share cap’ for TPAPs in 2021. The market share cap rule proposed that “total volume of transactions originated through TPAP shall not exceed 30 % of the total volume of transactions processed on UPI during the preceding three (3) months on a rolling basis.”

Although the NPCI9 has shelved its proposal to cap the volumes that can originate from TPAPs for now, there are two reasons why dominance of the top 2, 3 TPAPs is a significant commercial and regulatory issue.

Innovation in the ecosystem. TPAPs super-charged the ‘UPI movement’. Exclude that niche (hypothetically) and the PSPs participating in the UPI transaction chain are banks- not a participant that has demonstrated interest in growing the UPI ecosystem of themselves. So, whether the market share cap rule is enforced or otherwise may potentially have a bearing on UPI system itself, given the top 2 or 3 TPAPs could be expected to originate a disproportionately large number of transactions relative to the proverbial long tail of TPAPs.

Regulators believe that this dominance increases what they term concentration risk in the system.

Solutions for Reducing Dominance

Taxing Power as a Potential Solution

The logic of a tax is as follows. There’s concentration risk in the system because of T2 Apps. That's a ‘cost’ or ‘externality’ (to use the language of economists) that the T2 Apps impose on the system.

Classic public policy solutions recommend any externality can be solved by imposing a ‘tax’ (in this context, that ‘tax’ can be a countervailing levy (tax) on T2 Apps. As would be apparent, the tax solution to mitigating the concentration risk is just a better version of volume caps that are already on the table.

The tax collections can be distributed among other TPAPs in proportion to their market share. That ‘grant fund’ will allow them to invest it in growing their market share through the devices they seem fit.

The tax will be assessed beyond a defined threshold of transactions on the T2 Apps. One potential baseline for the trigger of the tax is the 30 % volume defined by the NPCI. The NPCI has transparency over the transaction origination information. So, administration of the tax may be a trivial issue.

International payment friendliness & acceptance

Speaking purely from my (Trupti’s) first hand experience - I don’t have an Aadhar card (Identity card - SSN card equivalent for India) that is linked to a bank account (one of the core requirements for signing up and linking funding source to UPI) so I used my International CC or even better- Cash for purchasing things in India. However, quite a few POS systems are designed to not accept International CCs, so that didn’t work. (Card fees, International card fees , FX etc. deters merchants to enable it). I always carried cash anticipating such scenarios but then you end up holding the line in supermarkets or in many cases I was told “Pay in cash only if you have exact change. You are my first cash customer so I don’t have any bills to give you back. My petty cash box is empty”. Now that the domestic population is set & on a good trajectory, maybe UPI should be opened up to international tourists by enabling UPI linkage to international CC or banks. Without that it becomes very difficult to navigate this fully digitized web with cash.

Having said that, ~ 1 yr ago, people from 10 countries in G20 (Singapore, USA, Australia, Canada, HK, Oman, Qatar, Saudi Arabia, UAE & UK) can access UPI by converting their money into UPI wallet at the airport. However, you can only do that at select International Airports. If you miss doing that at the airport or the airport you land is not part of this select list, you will have an experience like me.

In closing, UPI is a clear success story and holds forth as a template for designing RTPs. The next stage of its evolution lies in unlocking the next 300 million users consistent with broad-basing growth across a cross section of TPAPs. Implementing the solutions outlined by Mandar, we believe, potentially holds the key to achieving these objectives.

Where payment systems typically face the ‘cold start’ problem.

See https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1973082&ref=indiatech.com (PIB release of October 30, 2023)

https://cmrindia.com/india-smartphone-market-resilient-in-q4-2023-19-yoy-growth-65-5g-smartphones-shipped-cmr/

INR 10k-13k (India Mobile Handset Market Review Report Q423)

Worldline Payments Report, 2023

As we were putting this post together, The RBI in the Statement of Regulatory Policies issued with the last monetary policy statement announced auto replenishment feature on UPI lite. That will remove one source of friction inhibiting its use. See https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=58051 (Item 5)

NBFCs as they are commercially referred to. NBFCs are Indian variants of bank-like vehicles. The difference is that they have no default access to retail (low cost) deposits. They were envisaged to proliferate credit and typically rely on short tenor or dated securities on the liabilities side to fund the assets.

Third Party Payment Applications. These are Fintechs that integrate with the banking layer(s) (typically through a nodal bank and offer the interface through which the user transacts on UPI. See https://www.npci.org.in/what-we-do/upi/roles-responsibilities (for the role TPAPs play).

National Payment Corporation Of India, the umbrella retail payment system operator authorized by the RBI to operate retail payment systems including IMPS, Rupay and UPI protocol

Thank you for your thoughts, Shruti.

You are right- the lack of trust is the key inhibitor across form factors when it comes to reaching the next 300 m users. There are no easy solutions to achieving penetration. The ecosystem will have to pull all stops to engender trust and awareness and couple that with enhancing user convenience and utility ( which is what the RBI did with the recent auto- load feature). Adjacently - NPCI does not presently break down UPI lite figures / estimates. It will help to get some sunlight there.

About MDR- we already have a template in MDR for debit cards. That template can be gainfully deployed in UPI context as well. If you recall, RBI used GST thresholds to differentiate between merchants in Debit card MDR ( merchants with Turnover below GST thresholds are exempted and those above it, paid MDR in proportion to the transaction subject to a INR cap). It's plain to see that smaller merchants will preserve their incentives to accept UPI in this model.

About credit as a hook, am glad we are in principle agreement. Connectivity may not be a big challenge IMV given India boasts of lowest data costs anywhere in the world. (At the same time HH credit : GDP for India is lower than comparable economies).

UPI lite - Penetration (of UPI usage) is still bad in the lowest level with household income less than 1L, UPI lite hasnt picked up there mostly because problem was never 4/6 digit pin, it was trust and connectivity, trust goes worse with UPI lite and connectivity is still not at par to increase penetration

Relax MDR restrictions - For a country with average UPI transaction amount 1500 (down from 1800) and subsequently still going down, the trend isnt helpful for merchants to pay MDR, they will levy this on the consumer who will end up with same issue as credit card, they will start using cash. for above 2000 P2M they started asking 1.1% interchange fee, if they dont even take that, tech systems will suffer, companies are already losing a lot in the race to maintain success rate of UPI transaction, once winner was Paytm and they took away its banking license so thats gone too

Credit as a hook - only thing that might work in favour of people but again u still need internet connectivity in rural areas to better penetration and then adoption